The timing couldn’t have been more fitting. On Tax Day 2026, trade policy expert Shawn Marie Jarosz of Trade Moves LLC took the PMMI Executive Leadership Conference stage to deliver a real-time briefing on tariffs and trade — and the message for packaging and processing manufacturers was clear: Not only isn’t the volatility over, for some, it may just be getting started.

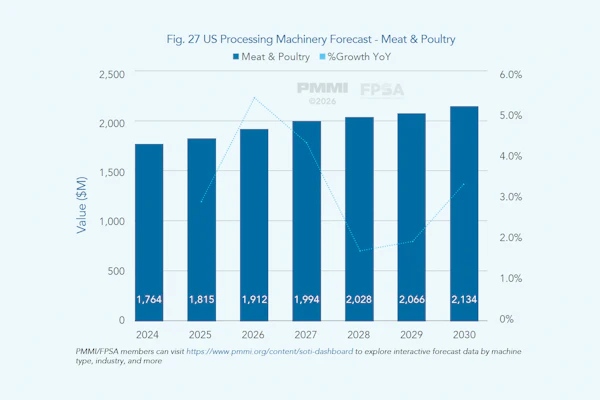

Cross-border trade is foundational to the packaging and processing sector. In 2025, the U.S. imported $7.1 billion worth of processing and packaging machinery (HS codes 8422 and 8438 alone), a figure that climbed to $7.3 billion in 2026, according to Jarosz. That’s before accounting for conveyors, industrial ovens, components, and other equipment that keep production lines running.

For an industry this deeply integrated into global supply chains, tariff policy isn’t an abstract concern — it’s a line item on every import invoice.

What just changed: IEEPA refund opportunities

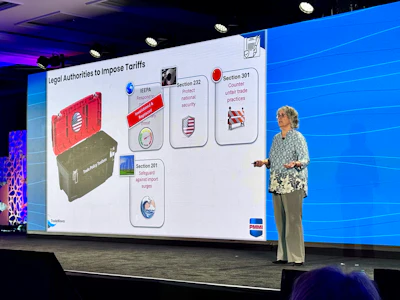

One of the most immediately actionable developments for packaging and processing importers is the invalidation of IEEPA (International Emergency Economic Powers Act) tariffs by the Supreme Court in February 2026. U.S. importers paid a staggering $175 billion in IEEPA tariffs — with small businesses accounting for roughly $55 billion of that total.

For the packaging and processing machinery sector specifically, an estimated $500 million in IEEPA tariffs may be eligible for refund, per Jarosz.

CBP (Customs and Border Protection) is launching a simplified, automated refund process on April 20th through the CAPE system within the ACE portal. Here’s what importers of record need to do:

- Set up ACH direct deposit with CBP — refunds will not be issued by paper check

- Gather entry numbers and submit them in CSV format through the CAPE system

- Track liquidation dates — entries liquidate 314 days after import, a critical window for eligibility

- Expect 60–90 days for processing, with interest included on refunded amounts

There is currently no deadline to apply, but Jarosz recommends that companies move quickly — and consult legal counsel about whether to file protective claims at the Court of International Trade in parallel, in case the process faces legal challenges.

One important downstream consideration: if you passed IEEPA tariff costs on to your customers, expect conversations about how refunds will be shared. Get ahead of it now.

Section 122 and more

IEEPA tariffs have been replaced by Section 122 global tariffs, currently set at 10%, but the president has signaled an increase to the statutory maximum of 15% before they expire in July 2026. Congressional extension is unlikely, given that both the Senate and House are reluctant to take ownership of tariff policy heading into the midterms.

What fills the gap after July? Jarosz expects a bridge to Section 301 and Section 232 tariffs, with multiple investigations already underway on accelerated timelines. The administration completed one Section 301 investigation in just four months—roughly the same window as the Section 122 tariff period.

The bottom line, according to Jarosz: plan for tariffs of 15–25% through the end of the current administration, i.e., Q4 2025 levels.

Steel, aluminum & the Section 232 shock

Perhaps the most significant near-term change for packaging and processing OEMs is the restructuring of Section 232 steel and aluminum tariffs. While the headline tariff rate has decreased, the new calculation method applies the tariff to the full value of the imported product—not just the value of the metal content. For high-value machinery, Jarosz explained that this is a critical distinction.

Consider this illustrative example:

Industrial Oven — $500,000 import value

Old Method | New Method | |

|---|---|---|

| Tariff basis | 20% metal value = $100,000 | Full product value = $500,000 |

| Tariff rate | 50% | 25% |

| Tariff cost | $50,000 | $125,000 |

| Delta | +$75,000 |

For a conveyor with higher metal content, the math may actually favor the new method, but every product will need to be evaluated individually.

Critically, the scope of Section 232 tariffs could expand. Currently, many categories, including industrial ovens, confectionery machinery, poultry processing equipment, and vaping machinery, are not subject to Section 232. But the administration retains the authority to broaden that scope at any time.

There is a silver lining, however, in the form of drawbacks. The ability to claim refunds on Section 232 tariffs for imported inputs that are manufactured into goods and subsequently exported is now available for the first time. For OEMs with significant export business, this is worth exploring with your trade counsel.

China & Section 301

Section 301 tariffs on Chinese goods have been a fixture of the trade landscape since the first Trump administration, and most companies have long since baked them into their cost structures. But a new wave of Section 301 investigations is underway.

The administration has targeted:

- 60 countries for insufficient enforcement of forced labor prohibitions in supply chains

- 16 markets — including Canada and the EU — for government-subsidized excess production capacity in sectors including food and beverage processing and industrial machinery

These investigations are moving fast. New tariffs could arrive just as Section 122 tariffs expire and according to Jarosz, that’s no accident.

USMCA: A critical lifeline, for now

For manufacturers with integrated North American supply chains, USMCA-compliant goods remain exempt from both IEEPA and Section 122 tariffs. In some cases, Canadian or Mexican-manufactured goods may actually carry a cost advantage over U.S.-made equivalents, since they avoid certain Section 232 surcharges.

But the USMCA trilateral review is underway, and the president has expressed interest in replacing the trilateral agreement with separate bilateral deals with Canada and Mexico. While a full withdrawal remains unlikely, the threat adds another layer of uncertainty for companies relying on North American supply chain integration.

Industry advocates — including PMMI — are pushing for limited changes to the agreement, stable rules of origin, and minimized Section 232 exposure on metal components.

What OEMs Should Do Now

With all of the moving parts, Jarosz outlined five concrete strategies for managing tariff exposure:

1. Apply for your IEEPA refund - If you imported processing or packaging machinery in 2025–2026, you may have money coming back. Set up ACH with CBP, pull your entry numbers, and file as soon as the CAPE system goes live on April 20th.

2. Audit your tariff classifications - If you’ve been importing under the same HTS code for 10–15 years, it’s time for a review. Product function, composition, and use may have changed — and the correct classification could mean the difference between being subject to Section 232 tariffs or not.

3. Scrutinize your dutiable value - CBP tariffs are assessed on the “price paid or payable” — but several cost components can be excluded:

- International freight and insurance (if documented separately)

- U.S.-based R&D or design costs

- Extended warranties

- U.S. installation costs

- Commissions paid to U.S.-based agents

4. Evaluate your sourcing strategy - With steel and aluminum prices elevated and transit disruptions ongoing due to the Iran/Middle East conflict, sourcing closer to home — from Canada, Mexico, or domestic suppliers — may offer resilience advantages beyond just tariff savings.

5. Prepare for customer conversations - If you’ve been passing tariff costs downstream, your customers will have questions about refunds, pricing adjustments, and future cost structures. Get ahead of these conversations now.