Brewers are looking for ways to reverse a contraction in sales, with strategies including diversifying product portfolios.

Pramote Polyamate via Getty Images

The competitive force of craft cocktails is growing, as craft brewers look to reverse a contraction in sales, according to PMMI Business Intelligence’s “2024 Craft Beer and Spirits” report.

Business Intelligence researchers compiled the experiences of 132 craft beer and spirits industry professionals for the report, using an online survey and direct long-form interviews to gauge each category’s current outlook.

One of the most prominent areas where the two categories differ is the overall momentum of sales. While craft beer has struggled to find avenues of growth in recent years, craft spirits are riding a wave of popularity, propelling the industry to new heights.

“The fact that shipments are down 6.9% over the last year in the craft beer market, our biggest challenges will be to keep costs down, keep people interested in craft beer, and diversify into cider,” said one participating owner of a craft microbrewery.

In both beer and spirits, “craft” is defined as a producer that yields under 6 million barrels annually. A producer is considered “micro” if they yield under 15,000 barrels annually.

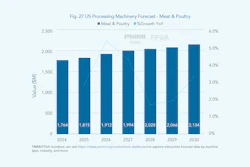

Craft brewing experienced unsustainable growth in the past decade, and it is now entering a phase of contraction.PMMI Business Intelligence: 2024 Craft Beer and Spirits - Success Through PackagingSales contraction in craft beer

After a decade of explosive and unsustainable growth, from 3,108 establishments in 2013 to 9,456 in 2023, craft beer has entered a phase of no growth and slight contraction, according to a 2023 “National Beer Sales & Production Data” report from the Brewers Association.

These numbers are in line with performance in recent years, signaling a new phase of essentially flat growth for craft beer.

This does not come as a surprise for the industry, with wholesalers telegraphing declining sales numbers in early 2023 when they predicted a 15-20% drop in overall orders, as explained in the BevNET article by Zoe Licata, “Craft Beer Overview: A ‘Culling’ of Craft is Coming.”

Several factors have coalesced to drive this shift away from growth in craft beer, from market saturation to changing consumer preferences, and the trend is expected to continue for at least a few years.

Despite this contraction in sales, the first half of 2023 still saw slightly more brewery openings than closings, the Brewers Association’s “National Beer Sales and Production Data” report said.

“Craft beer [growth] is somewhat flat; the biggest growth is in ready-to-drink cocktails in a can. The trend toward cans has been significant for a while,” said a partner for a beer and spirits contract packager with a yield between 15,000 and 79,000.

Craft spirits on the rise

Ready-to-drink cocktails in a can are contributing to growth in craft spirits.PMMI Business Intelligence: 2024 Craft Beer and Spirits - Success Through PackagingIn contrast to craft beer, craft spirits have entered a phase of robust growth.

Buoyed by the ascendant spirit-based pre-mixed cocktail segment and harnessing a shift in consumer preference away from beer and malt-based drinks, craft spirits are expected to continue healthy growth for the next several years with sustained double-digit compound annual growth rate (CAGR) predicted.

A key achievement for the craft spirit industry has been successfully taking share within the larger alcohol category away from craft beer, a feat that the craft beer industry has not quite figured out how to reciprocate.

SOURCE: PMMI Business Intelligence, 2024 Craft Beer and Spirits – Success Through Packaging

Craft brewing experienced unsustainable growth in the past decade, and it is now entering a phase of contraction.PMMI Business Intelligence: 2024 Craft Beer and Spirits - Success Through Packaging

Craft brewing experienced unsustainable growth in the past decade, and it is now entering a phase of contraction.PMMI Business Intelligence: 2024 Craft Beer and Spirits - Success Through Packaging Craft brewing experienced unsustainable growth in the past decade, and it is now entering a phase of contraction.PMMI Business Intelligence: 2024 Craft Beer and Spirits - Success Through Packaging

Craft brewing experienced unsustainable growth in the past decade, and it is now entering a phase of contraction.PMMI Business Intelligence: 2024 Craft Beer and Spirits - Success Through Packaging

Ready-to-drink cocktails in a can are contributing to growth in craft spirits.PMMI Business Intelligence: 2024 Craft Beer and Spirits - Success Through Packaging

Ready-to-drink cocktails in a can are contributing to growth in craft spirits.PMMI Business Intelligence: 2024 Craft Beer and Spirits - Success Through Packaging